All Categories

Featured

Table of Contents

There is no payment if the plan ends before your fatality or you live beyond the policy term. You might be able to restore a term policy at expiration, but the costs will be recalculated based on your age at the time of renewal. Term life insurance policy is typically the the very least costly life insurance policy offered because it provides a death benefit for a limited time and does not have a cash money value element like permanent insurance policy.

At age 50, the costs would climb to $67 a month. Term Life Insurance policy Fees 30 years old $18 $15 40 years old $28 $23 50 years old $67 $51 Source: Quotacy. Quotes are for a $250,000 30-year term life plan, for men and ladies in exceptional wellness.

Adjustable Term Life Insurance

Interest rates, the financials of the insurance firm, and state policies can also impact premiums. When you take into consideration the amount of coverage you can get for your costs bucks, term life insurance coverage tends to be the least expensive life insurance coverage.

Thirty-year-old George intends to shield his family members in the unlikely occasion of his sudden death. He gets a 10-year, $500,000 term life insurance coverage policy with a costs of $50 per month. If George dies within the 10-year term, the plan will pay George's recipient $500,000. If he dies after the plan has expired, his beneficiary will receive no benefit.

If George is identified with a terminal illness throughout the first plan term, he most likely will not be qualified to restore the plan when it expires. Some policies provide guaranteed re-insurability (without evidence of insurability), but such features come with a higher cost. There are a number of types of term life insurance coverage.

Most term life insurance coverage has a degree costs, and it's the kind we've been referring to in many of this post.

Universal Life Insurance Vs Term Life Insurance

Term life insurance policy is attractive to youths with kids. Moms and dads can get substantial coverage for an affordable, and if the insured dies while the policy is in effect, the family can count on the survivor benefit to change lost earnings. These plans are likewise appropriate for individuals with growing families.

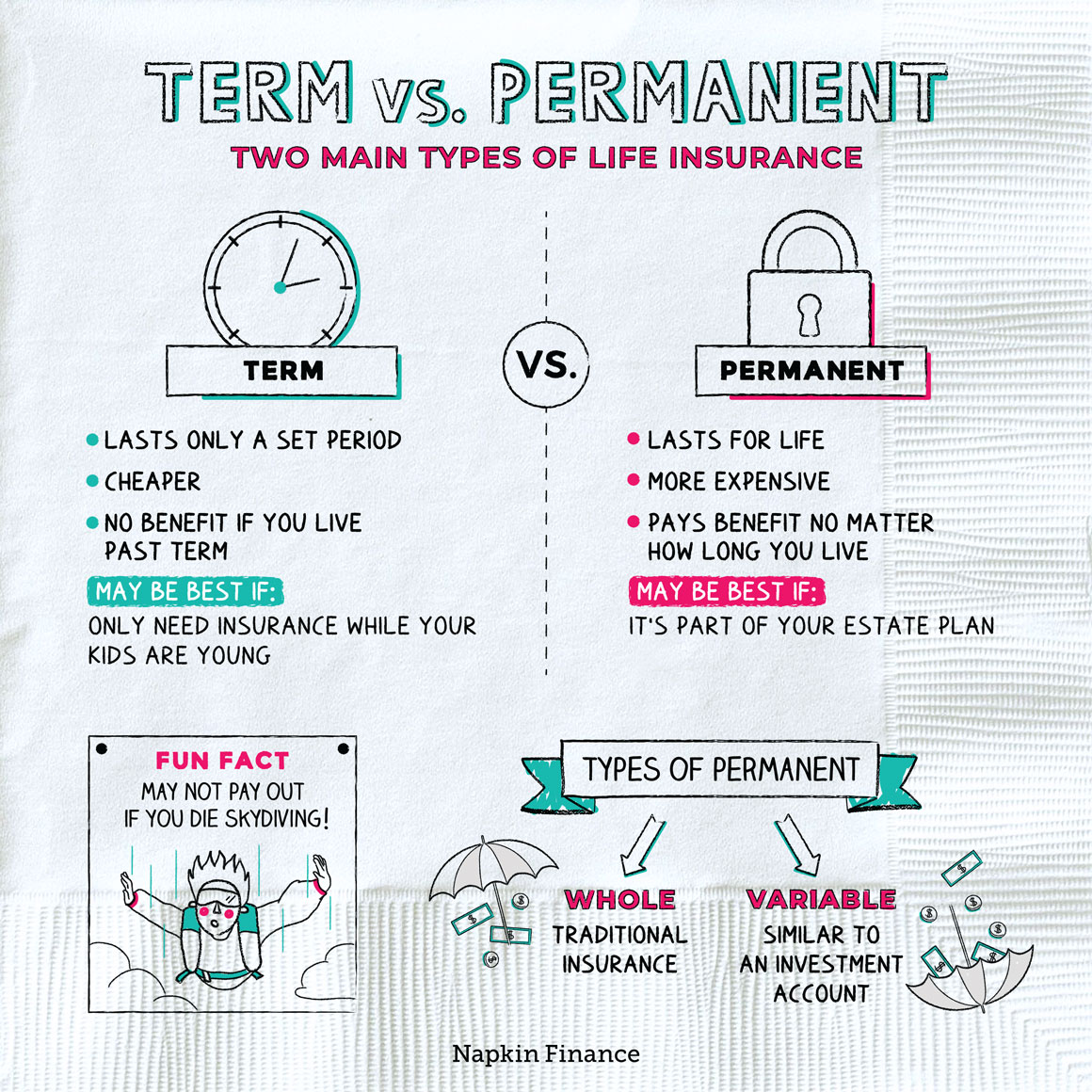

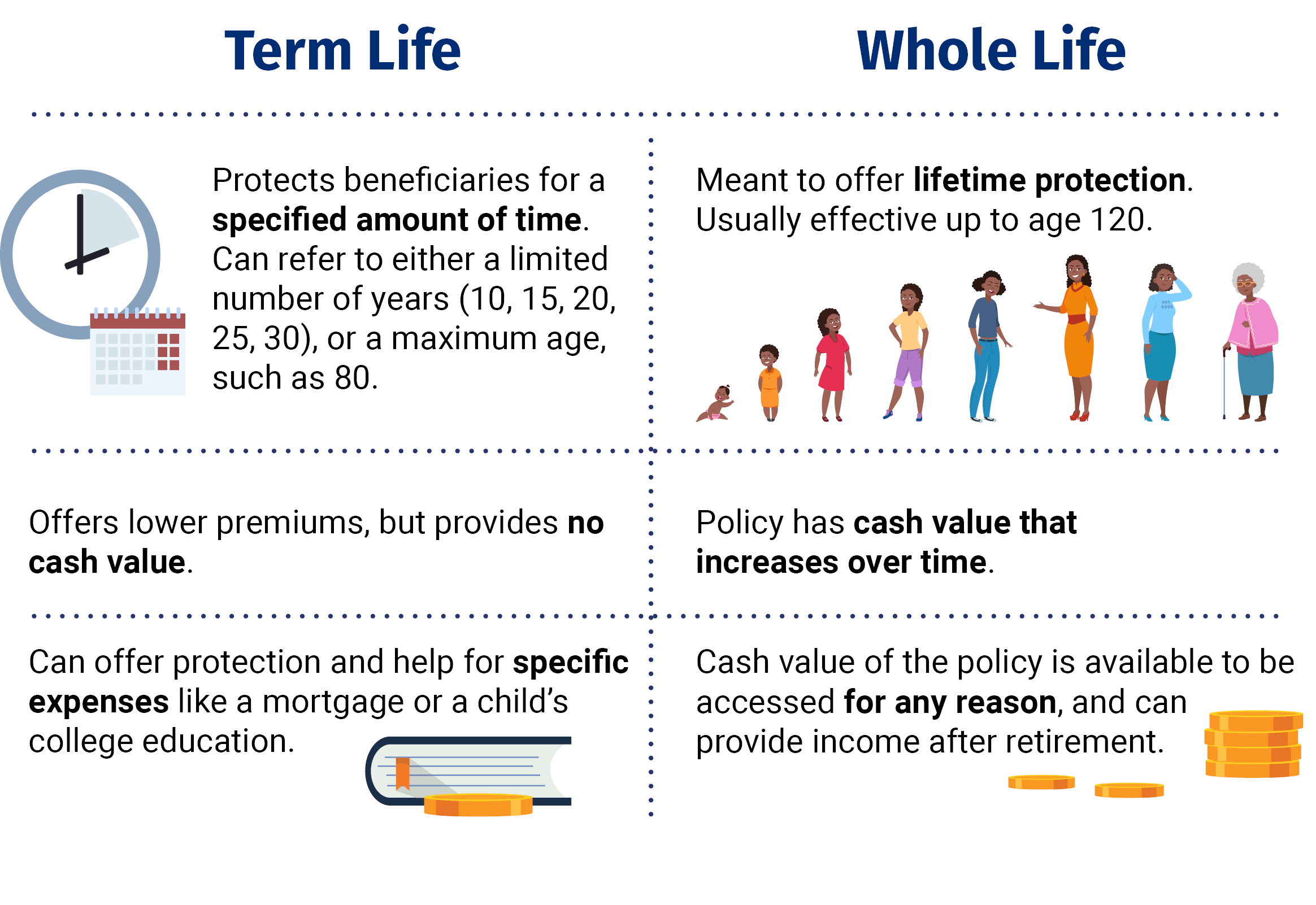

Term life plans are optimal for people who desire substantial coverage at a reduced price. People that possess entire life insurance coverage pay much more in costs for much less coverage yet have the safety of understanding they are safeguarded for life.

The conversion rider must enable you to transform to any permanent policy the insurance provider provides without limitations - spouse term rider life insurance. The key functions of the motorcyclist are keeping the initial health and wellness ranking of the term plan upon conversion (also if you later have wellness issues or come to be uninsurable) and determining when and just how much of the protection to transform

Of training course, overall costs will enhance considerably since entire life insurance policy is more pricey than term life insurance policy. The benefit is the guaranteed authorization without a medical test. Clinical problems that create throughout the term life period can not trigger premiums to be boosted. The firm may call for minimal or complete underwriting if you want to include additional bikers to the new plan, such as a long-term care motorcyclist.

Whole life insurance policy comes with substantially greater regular monthly costs. It is meant to provide protection for as long as you live.

Best Term Life Insurance In Uae

It depends upon their age. Insurance coverage companies set an optimum age limit for term life insurance policy plans. This is usually 80 to 90 years old but may be greater or lower depending upon the business. The costs additionally climbs with age, so an individual aged 60 or 70 will certainly pay substantially more than somebody years younger.

Term life is rather comparable to vehicle insurance. It's statistically not likely that you'll require it, and the premiums are money down the drainpipe if you don't. If the worst takes place, your family will get the advantages.

This policy design is for the consumer who requires life insurance policy but would love to have the capability to pick exactly how their cash value is invested. Variable plans are financed by National Life and distributed by Equity Solutions, Inc., Registered Broker/Dealer Affiliate of National Life Insurance Policy Company, One National Life Drive, Montpelier, Vermont 05604.

For J.D. Power 2024 award details, check out Permanent life insurance establishes cash worth that can be borrowed. Policy finances accumulate rate of interest and unsettled plan car loans and interest will certainly lower the fatality advantage and cash money worth of the plan. The quantity of cash value offered will typically depend on the kind of irreversible plan bought, the amount of protection bought, the size of time the policy has been in force and any kind of outstanding policy lendings.

Term Life Insurance Singapore

Disclosures This is a general description of coverage. A total declaration of insurance coverage is located only in the policy. For even more details on coverage, expenses, restrictions, and renewability, or to look for insurance coverage, contact your local State Farm agent. Insurance coverage and/or linked cyclists and functions may not be available in all states, and policy terms and problems may vary by state.

The primary differences in between the various types of term life plans on the market relate to the length of the term and the coverage quantity they offer.Level term life insurance coverage features both level costs and a degree survivor benefit, which means they stay the same throughout the period of the plan.

It can be renewed on an annual basis, but premiums will increase whenever you restore the policy.Increasing term life insurance policy, additionally referred to as a step-by-step term life insurance policy strategy, is a plan that comes with a death benefit that boosts gradually. It's typically a lot more complicated and pricey than level term.Decreasing term life insurance coverage features a payment that reduces with time. Common life insurance coverage term lengths Term life insurance policy is cost effective.

The major distinctions between term life and whole life are: The size of your coverage: Term life lasts for a set period of time and after that runs out. Ordinary monthly entire life insurance policy rate is calculated for non-smokers in a Preferred wellness classification, getting a whole life insurance policy paid up at age 100 offered by Policygenius from MassMutual. Aflac uses countless long-lasting life insurance plans, consisting of whole life insurance coverage, final expense insurance coverage, and term life insurance policy.

{kind=link}

Latest Posts

Ing Term Life Insurance Quote

Mississippi Term Life Insurance

Final Expense Insurance For Seniors Over 80